As a business owner, you have two options to defer paying taxes on profits: leaving extra money in the corporation or withdrawing it and investing in a Registered Retirement Savings Plan (RRSP). To invest in an RRSP, you need enough contribution room, determined by 18% of your salary income from the previous year, with a maximum of $30,780

In 2023, most provinces and territories will have a low tax cost for business income. However, there is a slight difference between SBD Income (active business income eligible for the small business deduction) and General Income (excluding active business income not eligible for the SBD).

Generally, paying taxes on dividends instead of salary results in a higher combined tax paid by the corporation and shareholder. This is true across all provinces and territories except New Brunswick, where paying taxes on dividends rather than salary results in a 0.51% tax saving.

For business owners with excess profits, investing in an RRSP may be more appealing than leaving the funds in the corporation. However, before doing so, one must have enough RRSP contribution room, determined by 18% of income earned in the preceding year, with a cap of $30,780 for 2023.

Regarding distributing corporate income, two options are available: salary or dividend. Depending on which is chosen, different tax implications can arise for those receiving a bonus vs dividend in Canada.

When it comes to salary, the individual pays personal tax. The taxation of dividends involves the corporation paying corporate tax on earned income and the individual paying personal tax on the proceeds when distributed as dividends, including taxes on dividends.

Corporate and personal tax rates should be integrated to ensure equal taxation for salaries and dividends, regardless of whether they receive a bonus vs dividend in Canada.

An example

Sera, a professional from Ontario, has incorporated her practice and is now an employee of the corporation. She has earned $190,000 of SBD Income in the past and distributed all of it as salary. After contributing to her RRSP and paying personal taxes, she spent the remaining funds on personal expenses.

Currently, Sera is contemplating two options for distributing the SBD Income from her corporation:

Salary / RRSP

Sera used the excess funds after maximizing her RRSP contribution and paying personal tax to cover her expenses. Historically, her corporation distributed all income as salary and invested the funds to yield a 5% return.

For 2023, Sera has decided to distribute all the SBD Income as salary. She plans to contribute $30,780 to an RRSP and use the remaining funds to pay her taxes. Sera will rely on withdrawals from either an RRSP or Registered Retirement Income Fund (RRIF) to finance her retirement spending when she retires.

Corporate investing/dividends

In 2023, Sera allocated a portion of her SBD Income as a salary to cover her expenses. After taxes, the remainder will be kept in the corporation for investment purposes. Any after-tax business and investment income will be distributed as dividends to fund her retirement spending.

According to Figure 3, if Sera invests $30,780 in her RRSP with a 5% rate of return over 30 years, it will grow to $133,029. After withdrawing and paying $63,853 in taxes, she will be left with $69,176

After 30 years of investing her after-tax SBD income in her corporation, the amount Sera will have varies depending on the income earned. For example, with interest, she would have $43,818; eligible dividends, $60,263; annually-realized capital gains, $69,494; and deferred capital gains, $82,226.

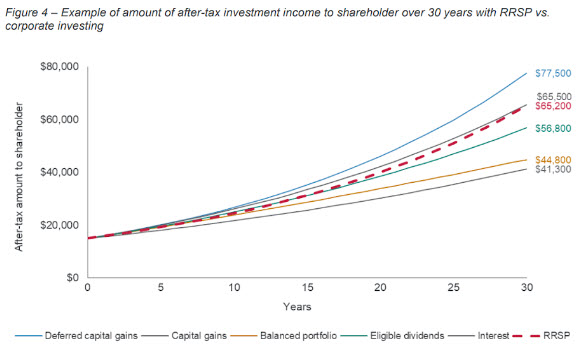

The calculation of Sera’s post-tax investment income over 30 years is shown in Figure 4. The calculation is based on the 2023 federal/Ontario bonus tax rates and a 5% rate of return, considering different types of income such as interest, eligible dividends, annually realized capital gains, deferred capital gains, and a balanced portfolio.

Several interesting trends emerge when comparing investing in an RRSP with corporate investing over 30 years.

- Interest: Investing in an RRSP always yields a better result than corporate investing.

- Eligible dividends: Initially, after-tax cash is slightly higher with corporate investments. However, after 15 years, an RRSP outperforms corporate investments.

- Annually-realized capital gains: Corporate investing always outperforms an RRSP.

- Deferred capital gains: Corporate investing always outperforms an RRSP.

- Balanced portfolio: Initially, after-tax cash is slightly higher with corporate investments. However, after six years, an RRSP outperforms corporate investments.

Impact of changes in personal tax rates on withdrawal

The taxation of RRSPs and corporate investments differs, which can substantially impact your after-tax returns. RRSPs are generally more advantageous over the long term, except when all your gains come from capital gains.

Other considerations

Regarding taxation, small businesses may encounter limitations on their deductions if their passive income or taxable capital exceeds certain thresholds. In particular, this deduction is restricted when passive income surpasses $50,000, or taxable capital surpasses $10 million.

CPP/QPP

- The employer and employee must contribute 5.95% of their wages towards CPP/QPP, with a yearly limit of $66,600 and the first $3,500 of earnings being exempt from contributions.

- While receiving salary payments can help maximize CPP/QPP entitlements, private investing is another option to consider for potentially higher pension income in the future.

EI Premiums

- EI premiums are not typically a worry for business owners with more than 40% of the company’s voting shares. They can use the tax credits and deductions available as majority shareholders.

- For those with 40% or less ownership, Employment Insurance premiums are applicable and will reach a cap of $2,406 when insurable earnings surpass the amount of $61,500

- Employers within specific regions of Canada can expect to face additional payroll taxes.

Lifetime Capital Gains Exemption (LCGE)

- In 2023, there was a limit of $971,190 for the disposition of qualified small business corporation (QSBC) shares.

- QSBC shares are desirable because they belong to Canadian-controlled private corporations where 90% or more of the assets are used in an active business.

- Excess funds in the company can jeopardize its QSBC status. However, purification can rectify this situation by distributing non-active assets, settling debts, or transferring assets to a related business.

RRSP Contributions for Income Splitting

- In the withdrawal phase of an RRSP, it is possible to split income with a spouse or partner.

- At 65, individuals can take advantage of income splitting through RRF withdrawals.

Dividend Payments for Income Splitting

- Distributing dividends to family members may trigger income-splitting rules.

- The federal government has introduced the Split Income (TOSI) rules.

- Dividend payments can allow income splitting with a non-working spouse or partner once they reach 65.

Loss of Small Business Deduction (SBD)

- There is a decrease in the SBD limit for taxable capital employed in Canada between $10M and $15M.

- The corporation’s adjusted aggregate investment income (AAII) can affect the availability of SBD. By adjusting the AAII, the level of accessibility to SBD may be altered.

- By removing funds from the corporation and investing in RRSPs, it is possible to maintain AAII and still be eligible for SBD.

Corporate Life Insurance

- Permanent life insurance policies owned by a corporation can effectively reduce annual taxes.

- The tax-deferred accumulation of value can increase the death benefit payout.

- When an individual expires, the corporation receives tax-exempt life insurance benefits and a credit to its capital dividend account.

- Permanent life insurance policies classified as “exempt” can be a useful tool for reducing the impact of SBD on passive income and minimizing potential losses.

- A strategy is available for individuals aged 45 and older who are in good health and have extra funds in their business. This strategy offers tax advantages and increases the value of their estate.

Conclusion

When choosing between a bonus vs dividend in Canada, it is important to consider the bonus tax rate and taxes on bonuses. Corporate income taxation, whether distributed through salary/bonus or dividends, may vary depending on the type of income and the province/territory where the business is situated. While there may be no significant tax savings or cost across all provinces and territories for SBD income, General Income may result in a tax cost ranging from 0.27% to 7.54%, except for New Brunswick, which offers tax savings of 0.51%.

FAQs

- What is a dividend for a business owner?

Distributing dividends allows business owners to regularly give back to their shareholders by distributing a portion of the company’s profits.

- What are the advantages of dividends?

Paying company dividends can provide shareholders with a consistent source of income, making it an attractive option for potential investors. Moreover, it enables business owners to maintain company ownership while raising capital without surrendering equity.

- How do dividends work for small businesses?

When running a small business, it is essential to consider the tax implications of distributing profits to the owner and shareholders through dividends. Speaking with a tax professional is highly recommended so that all relevant laws are followed correctly.

- Is a dividend better than a bonus?

When choosing between a dividend and a bonus, several factors must be considered, such as the tax rate on each type of income, the business owner’s financial situation, and the company’s goals. In general, dividends are taxed at a lower rate than bonuses, making them a more tax-efficient option in many cases.

- What are examples of dividends in business?

Stock buybacks, one-time special dividends, and recurring payments to shareholders are all forms of dividends in business. The tax implications of various dividend types should be thoroughly assessed, and consulting a tax expert may be necessary.